Solid Start to FY ’26; Raising Price Target from $4.50 to $5.00

DHI Group (DHX) reported Q1 ’26 results ahead of our estimates and consensus. The revenue upside was wholly attributable to the recent acquisition of Point Solutions Group. Organically, both revenue and bookings for ClearanceJobs and Dice were generally consistent with our expectations and reflected the same dynamics seen last quarter, namely modest growth for the former and declines for the latter. Trends in the company’s key customer metrics were also roughly in line with our assumptions, although churn among smaller customers was somewhat elevated. Gross margin was well ahead of our assumption despite the inclusion of Point Solutions Group’s staffing services revenue, and operating expenses came in lower than we modeled. As such, both adjusted EBITDA and non-GAAP EPS easily exceeded our estimates and consensus.

As anticipated, management raised its FY ’26 revenue guidance to account for the acquisition of Point Solutions Group in March. Absent that, guidance would have remained unchanged. As it stands, the acquisition adds $6.0 million in revenue and $1.5 million in adjusted EBITDA to FY ’26, although we surmise the latter figure includes some of the outperformance realized in Q1. We increase our estimates for this year and next in accordance. We continue to expect growth at ClearanceJobs to accelerate in the near-term driven by a significant increase in defense spending, and we remain cautiously optimistic in the prospects for further stabilization at Dice given a notable inflection in new job postings exiting Q1.

Reflecting the solid start to the year and the accretive impact of Point Solutions Group, we raise our price target from $4.50 to $5.00. We continue to derive our price target based on a FY ’26 EV/Sales multiple of 2x. Between management’s focus on free cash flow generation, strategic investments to expand the breadth and depth of the ClearanceJobs platform and return of capital to shareholders via share repurchases, we believe the market will ultimately recognize the value inherent in DHI Group’s businesses.

Exhibit I: Reported Results and Guidance Versus Expectations

Sources: DHI Group; K. Liu & Company LLC; FactSet Estimates

Q1 revenue of $29.7 million (-5.4% Y/Y) was above our estimate of $29.2 million and consensus of $29.1 million. The upside relative to our model was attributable to the acquisition of Point Solutions Group, which contributed approximately $0.7 million to the top line. Both ClearanceJobs revenue of $14.0 million (+4.6% Y/Y) and Dice revenue of $15.7 million (-17.1% Y/Y) were slightly ahead of our $13.7 million and $15.5 million estimates, respectively.

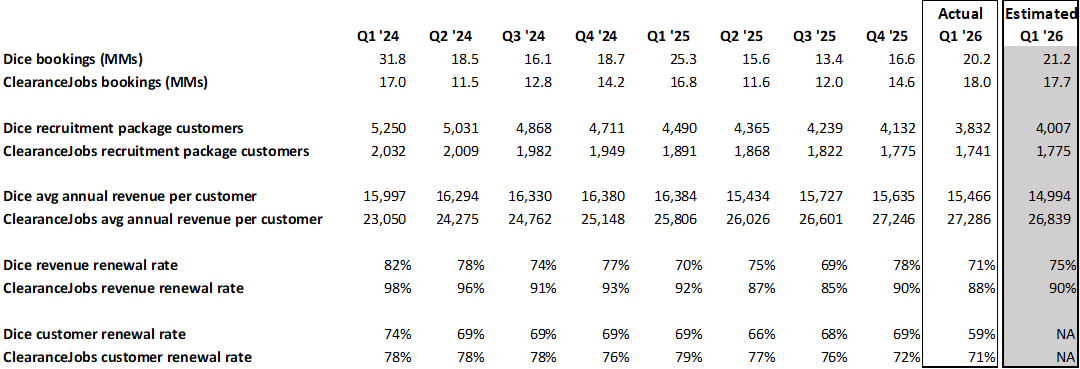

ClearanceJobs bookings of $18.0 million (+7.3% Y/Y) were slightly above our $17.7 million projection due to the inclusion of Point Solutions Group. Dice bookings of $20.2 million (-20.1% Y/Y) fell short of our $21.2 million forecast as a result of higher churn among the company’s smaller customers. Similar to the past several quarters, average revenue per customer continued to tick up for both ClearanceJobs and Dice, while customer counts declined due to the loss of smaller customers paying less than $15,000 annually. We note that a portion of the losses reflected in the customer renewal rate arose from the migration of smaller customers to Dice’s new self-service platform. As customers on that platform pay monthly, those subscribers are excluded from the reported number of recruitment package customers, which by definition covers only those with annual contracts.

Exhibit II: Key Metrics

Sources: DHI Group; K. Liu & Company LLC

Gross margin of 84.0% was above our 82.9% assumption due to lower costs than we projected. Total operating expenses (excluding non-recurring expenses not projected in our model) were also below our estimate, primarily due to lower sales and marketing expenses. As a result, adjusted EBITDA of $8.1 million (27.4% margin) easily exceeded our $6.4 million estimate and the Street’s $6.3 million. Non-GAAP EPS of $0.08 also beat our estimate of $0.04 and the Street’s $0.03.

In Q1, DHI Group generated $6.8 million in cash flow from operations and used $1.6 million for capital expenditures. Cash at quarter-end totaled $3.0 million, while outstanding debt increased from $30.0 million to $33.0 million. During the quarter, the company repurchased approximately 1.5 million shares at a total cost of $3.8 million, leaving $6.4 million remaining under the current repurchase authorization.

Reflecting the acquisition of Point Solutions Group, management raised its FY ‘26 revenue guidance by $6.0 million to $124.0-$128.0 million and reaffirmed prior expectations for an adjusted EBITDA margin of 25%, implying a $1.5 million increase in adjusted EBITDA to $31.0-$32.0 million. For Q2, management’s guidance calls for revenue of $30.0-$32.0 million, which adjusted for the impact of Point Solutions Group was in line with our prior estimate of $30.1 and the Street’s $29.4 million.

Exhibit III: Estimate Revisions

Source: K. Liu & Company LLC

We raise our estimates for this year and next, primarily reflecting the recent acquisition of Point Solutions Group, partially offset by the impact of higher churn than modeled in Q1. On the whole, our assumptions for accelerating growth at ClearanceJobs and moderating declines at Dice remain intact, and we continue to believe the company is poised for a return to positive revenue growth and margin expansion in FY ’27.

Our report with model and disclosures is available here.

Disclosure(s):

K. Liu & Company LLC (“the firm”) receives or intends to seek compensation from the companies covered in its research reports. The firm has received compensation from DHI Group, Inc. (DHX) in the past 12 months for “Sponsored Research.”

Sponsored Research produced by the firm is paid for by the subject company in the form of an initial retainer and a recurring monthly fee. The analysis and recommendations in our Sponsored Research reports are derived from the same process and methodologies utilized in all of our research reports whether sponsored or not. The subject company does not review any aspect of our Sponsored Research reports prior to publication.