Reports Q3 ’25 Results Above Expectations and Raises FY ’25 Adjusted EBITDA Guidance

DHI Group (DHX) reported Q3 ’25 results above our estimates and consensus. Against our model, the revenue upside was wholly attributable to ClearanceJobs, which generated far more transactional revenue than we projected. Revenue at Dice was in line with our forecast. Gross margin also exceeded our assumption, while operating expenses were considerably lower, resulting in both adjusted EBITDA and non-GAAP EPS topping our estimates and consensus. Underlying the headline results, ClearanceJobs bookings met our recently reduced projection, while Dice bookings were short of our forecast due to a lower revenue retention rate. For the former, new business bookings were negatively impacted by the looming government shutdown, but this was anticipated to an extent. As for the latter, bookings continue to bounce along the bottom amid a tepid recovery in technology hiring.

Reflecting the outperformance in Q3, management raised its FY ’25 adjusted EBITDA guidance and maintained its previous revenue guidance, which implies Q4 revenue consistent with our prior estimate and consensus. At Dice, management continues to see signs of stabilization, most notably in the number of prospects coming into the funnel and a ramp in AI-related job postings. However, new job postings remain at considerably lower levels than seen in years past, suggesting a return to growth is not yet imminent. In the interim, a new platform with greater self-service capabilities is being rolled out, which we believe has the potential to improve net dollar retention rates and reduce the cost per acquired customer over the long-term. As for ClearanceJobs, management remains confident in reverting to higher growth rates once the government reopens and spending against the proposed $1.1 trillion U.S. defense budget begins to flow. The integration of AgileATS is progressing well with bundled offers already available to new and existing customers.

Although our estimates move higher for this year, we believe the lingering external factors impacting both Dice and ClearanceJobs warrant a more conservative posture on near-term bookings. Our expectations for stabilization at Dice and double-digit growth at ClearanceJobs have therefore been pushed out by several quarters, and we reduce our FY ’26 estimates in accordance. Our price target also declines from $5.00 to $4.50, representing an unchanged FY ’26 EV/Sales multiple of 2x. Despite the reset in our expectations, we continue to believe shares of DHX are significantly undervalued. We expect the reopening of the government and an ensuing step up in global defense spending next year to serve as catalysts for the stock.

Exhibit I: Reported Results and Guidance Versus Expectations

Sources: DHI Group; K. Liu & Company LLC; FactSet Estimates

Q3 revenue of $32.1 million (-9.0% Y/Y) was ahead of our $31.0 million estimate and consensus of $31.1 million. Dice revenue of $18.2 million (-15.2% Y/Y) was in line with our $18.1 million projection, while ClearanceJobs revenue of $13.9 million (+0.7% Y/Y) was well above our $12.9 million estimate.

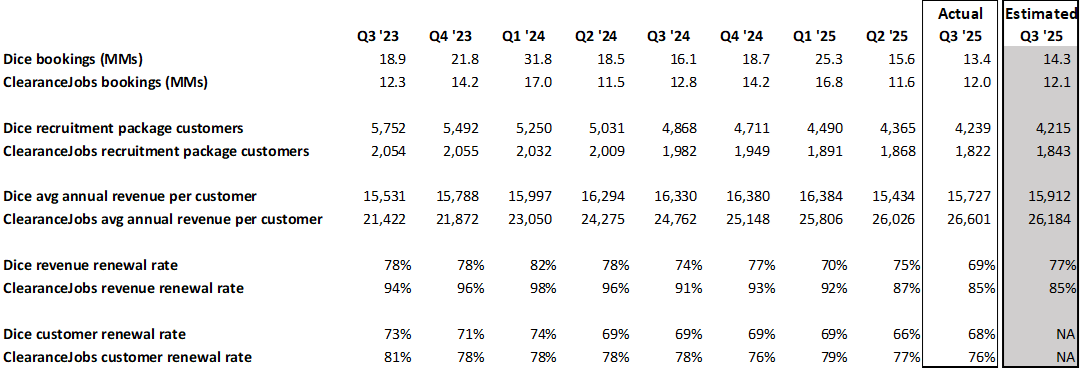

Dice bookings of $13.4 million (-16.6% Y/Y) were short of our $14.3 million projection, primarily due to a lower revenue renewal rate than we assumed. As in recent quarters, Dice churn was largely attributable to smaller customers spending less than $15,000 annually. That said, we were encouraged to see the customer count come in slightly ahead of our forecast, suggesting some moderation in the number of lost customers.

ClearanceJobs bookings of $12.0 million (-6.5% Y/Y) was approximately in line with our recently lowered $12.1 million projection. As anticipated, uncertainty arising from the looming government shutdown weighed on new business bookings. Revenue renewal rates trailed our assumptions due to the loss of smaller customers as well as one large government agency customer, but the impact on the bookings line was largely offset by higher transactional bookings than we projected. Looking forward, management remains optimistic that ClearanceJobs bookings will revert to higher growth rates given the anticipated increases in government defense budgets domestically and abroad.

Exhibit II: Key Metrics

Sources: DHI Group; K. Liu & Company LLC

Gross margin of 85.7% was well above our 83.8% assumption due to lower costs than we projected. Total operating expenses (excluding severance, professional fees and other non-recurring expenses not factored into our model) were also lower than we modeled, particularly on the sales and marketing line. As a result, adjusted EBITDA of $10.3 million (32.0% margin) easily exceeded our $9.0 million estimate and the Street’s $8.7 million. Non-GAAP EPS of $0.09 also beat our estimate of $0.08 and the Street’s $0.05.

In Q3, DHI Group generated $4.8 million in cash flow from operations and used $1.6 million for capital expenditures. Cash at quarter-end totaled $2.3 million, while outstanding debt remained unchanged at $30.0 million. During the quarter, the company repurchased 740,661 shares at a total cost of $2.1 million.

Management’s Q4 guidance calls for revenue of $29.5-$31.5 million. Prior to revisions, both consensus and our revenue estimate stood at $30.9 million. For FY ’25, management maintained its prior revenue guidance of $126.0-$128.0 million but raised its adjusted EBITDA margin target from 26.0% to 27.0%.

Exhibit III: Estimate Revisions

Source: K. Liu & Company LLC

Reflecting the outperformance in Q3, we raise our estimates for FY ’25. However, we lower our estimates for FY ’26 as we now assume a slower recovery in Dice bookings along with more conservative growth assumptions for ClearanceJobs bookings. In effect, our prior expectations for stabilization at Dice and double-digit growth at ClearanceJobs have been pushed out by several quarters. We therefore introduce our FY ’27 estimates, which reflect Dice and ClearanceJobs revenue growth rates commensurate with these assumptions, along with a full year adjusted EBITDA margin approaching 27%. Specifically, our FY ’27 estimates call for revenue of $128.7 million, adjusted EBITDA of $34.3 million and non-GAAP EPS of $0.28.

Our model with report and disclosures is available here.

Disclosure(s):

K. Liu & Company LLC (“the firm”) receives or intends to seek compensation from the companies covered in its research reports. The firm has received compensation from DHI Group, Inc. (DHX) in the past 12 months for “Sponsored Research.”

Sponsored Research produced by the firm is paid for by the subject company in the form of an initial retainer and a recurring monthly fee. The analysis and recommendations in our Sponsored Research reports are derived from the same process and methodologies utilized in all of our research reports whether sponsored or not. The subject company does not review any aspect of our Sponsored Research reports prior to publication.